How to Negotiate Your Credit Card Debt: A Step-by-Step Guide

How to Negotiate Your Credit Card Debt: A Step-by-Step Guide

Credit card debt can be overwhelming, but it's important to remember that you have options. Negotiating your credit card debt is a practical way to reduce what you owe and regain control of your finances. In this guide, we will walk you through the steps to successfully negotiate your debt, providing actionable advice along the way.

Understanding Credit Card Debt

Credit card debt arises when consumers borrow money from credit card companies to make purchases or withdraw cash. This debt typically comes with high-interest rates, making it challenging to pay off over time. The longer you carry a balance, the more you pay in interest, leading to a cycle of debt that can be difficult to escape.

Why Negotiate Your Debt?

Negotiating your credit card debt can provide significant financial relief. Here are a few reasons why you should consider negotiation:

- Reduce Your Debt: You may be able to settle for less than what you owe.

- Lower Interest Rates: Negotiation can lead to reduced interest rates, making it easier to pay off your debt.

- Flexible Payment Plans: You might negotiate a more manageable payment plan that fits your budget.

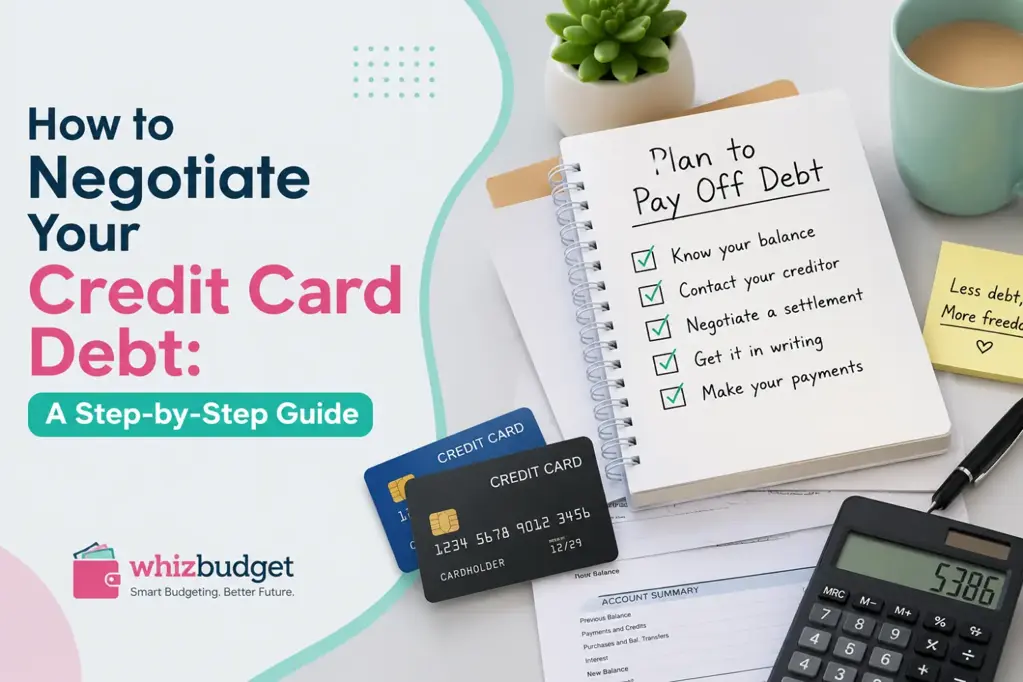

Step 1: Assess Your Financial Situation

The first step in negotiating your credit card debt is to have a clear understanding of your financial situation. Here’s how to do it:

- List Your Debts: Write down all your credit card debts, including the total amount owed, interest rates, and monthly payments.

- Calculate Your Income: Determine your total monthly income from all sources.

- Budget Your Expenses: Create a budget to understand your fixed and variable expenses. Use tools like WhizBudget to help you track your spending and identify areas where you can cut back.

By assessing your financial situation, you will have a clearer picture of what you can afford to pay in negotiations.

Step 2: Research Your Creditors

Understanding your creditors is crucial in the negotiation process. Here’s what you need to do:

- Know Your Creditor: Research your credit card issuer to understand their policies and practices regarding debt negotiation.

- Understand Their Willingness to Negotiate: Some creditors are more open to negotiation than others. Look for reviews or testimonials from other customers who have negotiated their debts.

- Gather Contact Information: Ensure you have the correct contact details for the debt collection department of your creditor.

Step 3: Prepare Your Negotiation Strategy

Preparation is key to successful negotiations. Consider the following strategies:

- Set a Target Amount: Decide the amount you wish to negotiate based on your financial assessment.

- Determine Your Position: Know the maximum amount you are willing to pay and stick to it.

- Prepare Your Case: Be ready to explain your financial situation and why you are unable to pay the full amount.

Your negotiation strategy should be realistic and grounded in your financial capabilities.

Step 4: Initiate the Negotiation

Once you are prepared, it's time to reach out to your creditor:

- Contact Them: Call the customer service number or send a written request to the debt collection department.

- Be Polite: Approach the conversation with respect and politeness. A positive attitude can go a long way.

- Present Your Case: Clearly explain your financial situation and your proposal for settlement or reduced payments.

Being calm and clear during negotiations can help facilitate a positive outcome.

Step 5: Finalize the Agreement

If your creditor agrees to your proposal, ensure that you finalize the agreement properly:

- Get Everything in Writing: Request a written confirmation of the new terms and conditions.

- Review the Agreement: Carefully read through the agreement to ensure there are no hidden fees or conditions.

- Follow Through: Make your payments on time as agreed to avoid reverting to the original terms.

Common Pitfalls to Avoid

Negotiating credit card debt can be tricky. Avoid these common pitfalls:

- Not Having a Budget: Without a budget, you may agree to payments you can’t afford.

- Being Unprepared: Going into negotiations without a clear strategy can lead to unfavorable outcomes.

- Ignoring the Fine Print: Always read the terms of any agreement before accepting it.

FAQs

What is debt negotiation?

Debt negotiation is the process of discussing with creditors to reduce the amount owed or to modify payment terms.

Will negotiating my credit card debt affect my credit score?

Yes, negotiating debt can impact your credit score, but it may be a necessary step to improve your financial situation.

How much can I expect to save through negotiation?

It varies, but many consumers are able to negotiate a reduction of 30% to 50% on their total debt.

Is it better to negotiate on my own or hire a professional?

It depends on your comfort level with negotiation. Hiring a professional can sometimes yield better results, but it also comes with costs.

What if my creditor refuses to negotiate?

If negotiations fail, consider other options like debt consolidation or seeking advice from a financial counselor.

Conclusion

Negotiating your credit card debt can be a daunting task, but with the right approach and preparation, you can achieve a more manageable financial situation. Remember to assess your finances, research your creditors, and prepare a solid negotiation strategy. Tools like WhizBudget can assist you in budgeting and tracking your expenses, making it easier to handle your debts. Start negotiating today and take the first step towards financial freedom!