The Ultimate Guide to Family Budgeting: Track Expenses & Save More

Managing family finances can feel overwhelming, but with the right tools and strategies, you can gain control and significantly reduce financial stress. A clear, well-structured budget helps you track spending patterns, identify areas to cut costs, and plan effectively for your family's future financial goals.

Why Family Budgeting is More Critical Than Ever

In today's economic climate, families face unprecedented financial challenges. From rising inflation to unexpected expenses, having a solid budgeting system isn't just helpful, it's essential for financial survival and growth.

The Real Cost of Not Budgeting

Without a proper budget, families typically overspend by 15-20% each month, according to financial experts. This translates to thousands of dollars in lost savings annually. Common consequences include:

- Accumulating credit card debt with high interest rates

- Missing opportunities to build emergency funds

- Inability to save for major goals like homeownership or college tuition

- Constant financial stress affecting family relationships

- Poor preparation for unexpected expenses like medical bills or car repairs

Benefits of Effective Family Budgeting

A well-implemented budget provides numerous advantages:

Financial Clarity: A budget gives you a comprehensive spending overview, showing exactly where your money flows each month. With detailed insights on your total balance across all accounts and spending patterns by category, you can identify trends, prevent overspending, and build substantial savings effortlessly.

Stress Reduction: When you know where every dollar goes, financial anxiety decreases dramatically. You'll sleep better knowing you have a plan and emergency funds.

Goal Achievement: Whether you're saving for a family vacation, a new home, or your children's education, budgeting makes these dreams achievable through systematic planning.

Teaching Opportunities: Involving children in age-appropriate budgeting discussions teaches valuable life skills and financial responsibility.

How to Create a Comprehensive Family Budget: Step-by-Step Guide

Step 1: Calculate Your Total Family Income

Start by documenting all income sources:

- Primary and secondary salaries (after taxes)

- Side hustles or freelance work

- Investment dividends or rental income

- Child support or alimony

- Government benefits or tax refunds

Pro Tip: Use your net income (take-home pay) rather than gross income for more accurate budgeting.

Step 2: Track Every Expense Meticulously

List all sources of income and log every expense, no matter how small. WhizBudget.com provides a detailed breakdown of your spending across multiple categories, helping you maintain complete oversight of your family finances.

Many families are surprised to discover where their money actually goes. That daily coffee run might seem insignificant, but it can add up to $1,500 annually.

Step 3: Categorise Your Spending for Better Control

Organise expenses into clear categories to see exactly how much you spend on:

Fixed Expenses (typically unchanging):

- Mortgage or rent payments

- Insurance premiums (health, auto, home)

- Loan payments (car, student, personal)

- Utilities (electricity, gas, water, internet)

- Subscription services

Variable Expenses (fluctuate monthly):

- Groceries and household supplies

- Transportation costs (gas, public transit)

- Entertainment and dining out

- Clothing and personal care

- Medical expenses and pharmacy costs

Savings and Investments:

- Emergency fund contributions

- Retirement account deposits

- College savings plans

- Short-term goal savings

With monthly views in WhizBudget.com, you can review past spending patterns and make informed adjustments for future savings opportunities.

Step 4: Apply the 50/30/20 Rule for Family Budgeting

This popular budgeting framework allocates:

- 50% for needs (housing, utilities, groceries, minimum debt payments)

- 30% for wants (entertainment, dining out, hobbies)

- 20% for savings and extra debt payments

Adjust these percentages based on your family's specific circumstances and financial goals.

Step 5: Set Realistic Budget Limits

Once you understand your spending patterns, establish reasonable limits for discretionary categories. Focus on:

Grocery Budget Optimisation: Plan meals, use coupons, and shop sales. The average family can save $200-300 monthly with strategic grocery planning.

Entertainment Spending: Set a monthly entertainment budget and explore free family activities like hiking, library events, or community festivals.

Subscription Audit: Cancel unused subscriptions and negotiate better rates for services you keep.

Small, consistent adjustments lead to substantial savings over time.

Step 6: Build Your Emergency Fund

Financial experts recommend saving 3-6 months of living expenses for emergencies. Start small:

- Week 1-4: Save $25 per week

- Month 2: Increase to $50 per week

- Continue increasing as your budget stabilises

Step 7: Monitor, Review, and Adjust Regularly

Successful budgeting requires ongoing attention. Schedule monthly budget reviews to:

- Compare actual spending to budgeted amounts

- Identify problem areas or spending leaks

- Celebrate successes and progress toward goals

- Adjust categories based on changing family needs

With WhizBudget.com's comprehensive tracking tools, you can analyse spending trends over time and make data-driven financial decisions. You'll be able to look back months later and clearly understand your spending patterns, saying, "That's where my money went! I need to be more mindful about this category."

Advanced Family Budgeting Strategies

The Envelope Method for Cash Categories

Allocate cash for specific spending categories like groceries or entertainment. When the envelope is empty, you're done spending in that category for the month.

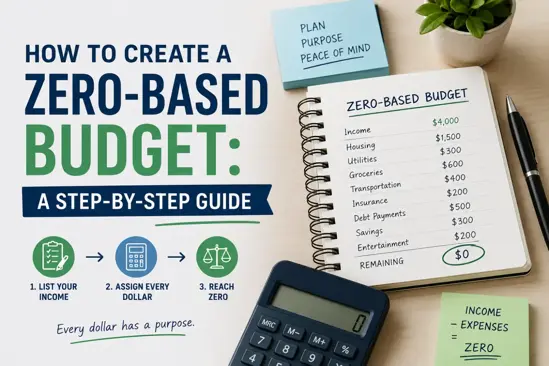

Zero-Based Budgeting

Assign every dollar a specific purpose before the month begins. Your income minus all assigned expenses and savings should equal zero.

Automated Savings

Set up automatic transfers to savings accounts immediately after payday. This "pay yourself first" approach ensures consistent saving.

Common Family Budgeting Mistakes to Avoid

1. Being Too Restrictive Initially

Overly strict budgets often fail. Allow some flexibility for occasional splurges to maintain long-term success.

2. Ignoring Small Expenses

Those $5 purchases add up quickly. Track everything to get accurate spending pictures.

3. Not Planning for Irregular Expenses

Budget for quarterly or annual expenses like car maintenance, holiday gifts, or school supplies.

4. Failing to Include All Family Members

Age-appropriate involvement helps everyone understand and support family financial goals.

5. Not Adjusting for Life Changes

Major life events (new baby, job change, moving) require budget modifications.

Teaching Children About Family Budgeting

Involving children in budgeting conversations provides valuable learning opportunities:

Ages 5-8: Use visual aids like jars for spending, saving, and giving. Explain needs versus wants during shopping trips.

Ages 9-12: Involve them in grocery budgeting. Give them a category budget and let them make choices within limits.

Ages 13-18: Discuss larger financial decisions and include them in family budget meetings. Consider giving them clothing or entertainment budgets to manage independently.

Technology Tools for Modern Family Budgeting

Digital budgeting tools streamline the process significantly:

Mobile Apps: Track expenses on-the-go and sync across family devices.

Bank Integration: Automatically categorize transactions and monitor spending in real-time.

Goal Tracking: Visualize progress toward savings goals and major purchases.

Reporting Features: Generate detailed spending reports to identify trends and opportunities.

WhizBudget.com integrates these essential features, making family financial management more accessible and effective than traditional spreadsheet methods.

Seasonal Budgeting Considerations

Spring Planning

- Tax refund allocation

- Home maintenance and landscaping

- Summer vacation planning

Summer Adjustments

- Increased utility costs from air conditioning

- Vacation and travel expenses

- Summer camp or childcare costs

Fall Preparation

- Back-to-school shopping and fees

- Holiday savings planning

- Heating cost preparation

Winter Management

- Holiday gift budgets

- Higher heating bills

- End-of-year tax planning

Overcoming Common Budgeting Challenges

Challenge 1: Irregular Income

For families with variable income (commission, freelance, seasonal work):

- Base budget on lowest expected monthly income

- Create separate savings for higher-income months

- Build larger emergency funds for income gaps

Challenge 2: Unexpected Expenses

When emergencies arise:

- Use emergency fund first

- Adjust other categories temporarily

- Consider additional income sources if needed

Challenge 3: Partner Disagreements

Resolve financial conflicts through:

- Regular budget meetings

- Compromise on spending priorities

- Individual "fun money" allowances

- Professional counselling if needed

Long-Term Financial Planning Beyond Budgeting

Retirement Savings

Even young families should prioritise retirement contributions:

- Take advantage of employer 401(k) matching

- Consider Roth IRA contributions for tax-free retirement income

- Start early to benefit from compound interest

College Savings

Education costs continue rising, making early planning crucial:

- Research 529 education savings plans

- Consider automatic monthly contributions

- Explore education tax credits and deductions

Insurance Planning

Adequate insurance protects your budget from catastrophic expenses:

- Life insurance to replace lost income

- Disability insurance for injury protection

- Adequate health insurance coverage

- Homeowner's or renter's insurance

Measuring Your Budgeting Success

Track these key metrics to evaluate your family's financial progress:

Debt-to-Income Ratio: Total monthly debt payments divided by gross monthly income. Aim for less than 36%.

Savings Rate: Percentage of income saved monthly. Target 20% or higher when possible.

Emergency Fund Coverage: Months of expenses covered by emergency savings. Build toward 3-6 months.

Net Worth Growth: Total assets minus total debts. Track quarterly to ensure steady progress.

When to Seek Professional Help

Consider consulting a financial advisor when:

- Struggling with significant debt

- Planning major life changes (retirement, divorce, inheritance)

- Needing investment guidance beyond basic savings

- Experiencing persistent financial stress despite budgeting efforts

Conclusion: Your Path to Financial Freedom Starts Today

Budgeting doesn't have to be complicated or restrictive. With the right approach and tools, family budgeting becomes an empowering habit that reduces stress and accelerates your progress toward financial goals.

WhizBudget.com makes comprehensive family budgeting accessible by providing intuitive expense tracking, real-time account balance monitoring, and detailed spending analysis by category—all integrated in one powerful platform. Our user-friendly interface helps families of all sizes and income levels take control of their financial futures.

Start your budgeting journey today and transform your family's financial outlook. With consistent effort and the right tools, you'll build lasting financial security and create opportunities for the experiences and goals that matter most to your family.

Remember: every financial expert started with a single budget. Your commitment to family financial planning today creates the foundation for decades of financial success and peace of mind.