Saving Strategies

Ways to cut costs and grow savings

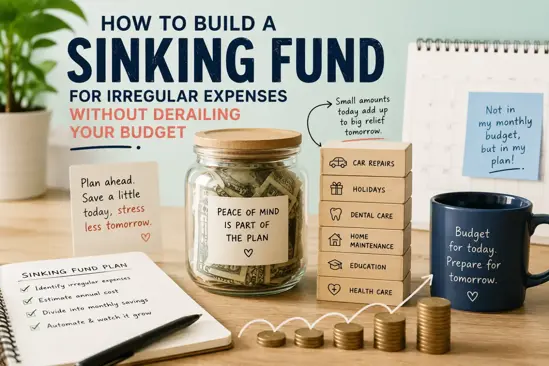

How to Build a Sinking Fund for Irregular Expenses Without Derailing Your Budget

How to Build a Sinking Fund for Irregular Expenses Without Derailing Your Budget

If your monthly budget looks fine on paper but falls apart whenever the car needs repairs, your insurance renewal arrives, or school costs pop up, you are not bad with money. You are probably just budgeting for a normal month and forgetting that real life is not monthly.

Many household costs in Europe are irregular. They may happen once a year, twice a year, seasonally, or without a neat pattern. Car maintenance, annual subscriptions, holidays, property taxes, medical co-payments, Christmas, back-to-school costs, vet bills, and insurance premiums can all disrupt your cash flow if you treat them as surprises.

A sinking fund for irregular expenses solves this problem. Instead of panicking when a large bill arrives, you save a smaller amount every month in advance. This article explains how to save for irregular expenses using simple formulas, realistic examples, and a practical system you can repeat every year.

What Is a Sinking Fund and Why It Matters

A sinking fund is money you set aside regularly for a specific future expense. The expense might be predictable, such as an annual car insurance premium, or semi-predictable, such as car repairs. The point is to spread the cost over time instead of letting it crash into one month.

For example, if your annual home insurance costs €480, you can save €40 per month. When the bill arrives, the money is already waiting. Your monthly budget stays stable, and you do not need to rely on a credit card, overdraft, or last-minute transfer from savings.

Sinking funds matter because they make your budget more honest. A monthly budget that ignores annual expenses is incomplete. You may think you have €300 left over each month, but if you have not accounted for Christmas, car service, insurance renewals, or holiday travel, that money is already partly spoken for.

The goal is not to make your budget more complicated. The goal is to make it more realistic. A good sinking fund system turns large, stressful costs into small, planned monthly savings amounts.

Sinking Fund vs Emergency Fund: Key Differences

A sinking fund and an emergency fund are both savings tools, but they are not the same. Mixing them together often causes problems. If you use your emergency fund for annual bills, it may not be available when a real emergency happens.

| Feature | Sinking Fund | Emergency Fund |

|---|---|---|

| Purpose | Planned or expected irregular expenses | True financial emergencies |

| Examples | Insurance premium, car service, holidays, school costs | Job loss, urgent medical cost, essential home repair |

| Timing | Often predictable or estimated | Unpredictable |

| Amount | Based on known future costs | Usually 3 to 6 months of essential expenses |

| How often used | Regularly throughout the year | Only when necessary |

Think of a sinking fund as your plan for known bumps in the road. Think of an emergency fund as your safety net when the road disappears entirely.

For example, replacing worn tyres is usually not an emergency if you knew they were getting old. It belongs in a car maintenance sinking fund. Losing your job and needing to cover rent or mortgage payments is an emergency fund situation.

Common Irregular Expenses You Should Plan For

The first step in budgeting for non monthly expenses is to identify the costs that do not fit neatly into your regular monthly bills. Start by looking through the past 12 months of bank statements and card transactions. Highlight every expense that was not part of your normal monthly routine.

Common sinking fund categories include:

- Car costs: servicing, repairs, tyres, MOT or roadworthiness tests, toll tags, parking permits, registration fees, and insurance excesses.

- Insurance premiums: car insurance, home insurance, life insurance, health insurance top-ups, travel insurance, and pet insurance if paid annually.

- Home and property: boiler servicing, appliance replacement, property tax, minor repairs, garden maintenance, and furniture replacement.

- Medical and dental: dental check-ups, glasses, prescriptions, physiotherapy, specialist appointments, and co-payments.

- Family and school costs: uniforms, books, school trips, childcare deposits, sports equipment, and exam fees.

- Holidays and travel: flights, accommodation, spending money, passports, luggage, and transport to the airport.

- Seasonal events: Christmas, birthdays, weddings, religious celebrations, and family visits.

- Subscriptions and memberships: annual software, gym membership, professional memberships, streaming renewals, and cloud storage.

- Pets: vaccinations, vet check-ups, grooming, pet boarding, and unexpected but non-emergency care.

You do not need 30 separate funds. Too many categories can become hard to manage. A useful approach is to group similar costs. For example, instead of separate funds for tyres, servicing, and repairs, you could use one car maintenance fund.

How to Calculate Your Monthly Sinking Fund Amount

The basic sinking fund formula is simple:

Total expected cost ÷ number of months until due = monthly sinking fund amount

If your car insurance is €720 and it is due in 12 months, the calculation is:

€720 ÷ 12 = €60 per month

If Christmas usually costs €900 and you have 9 months left to save, the calculation is:

€900 ÷ 9 = €100 per month

For expenses that are not exact, use a realistic estimate based on previous years. If you spent €550 on car repairs last year and €700 the year before, you might set a target of €650 or €700. It is better to slightly overestimate essential categories than to be short when the bill arrives.

For annual expenses budget planning, make a list with four columns:

- Expense category

- Expected annual cost

- Due date or likely timing

- Monthly savings amount

Here is a simple example:

| Expense | Expected Cost | Months to Save | Monthly Amount |

|---|---|---|---|

| Car insurance | €720 | 12 | €60 |

| Car maintenance | €600 | 12 | €50 |

| Christmas | €900 | 9 | €100 |

| School costs | €480 | 6 | €80 |

| Holiday travel | €1,200 | 12 | €100 |

In this example, the household needs to set aside €390 per month. That may feel high, but remember: these costs are happening anyway. The sinking fund simply reveals the true monthly cost of your lifestyle and commitments.

Step-by-Step Method to Set Up Your Sinking Fund

Use this process to build a system that is clear, repeatable, and easy to maintain.

- Review the last 12 months. Go through bank statements, credit card statements, and payment apps. List every irregular expense over €25 or €50, depending on your income level.

- Group expenses into categories. Use practical sinking fund categories such as car, home, insurance, school, holidays, gifts, medical, and pets.

- Estimate annual totals. Use last year as a guide, but adjust for price increases. In many European countries, insurance, travel, utilities, and food-related celebration costs have risen, so avoid using outdated numbers.

- Set target dates. If the cost has a fixed due date, write it down. If not, choose a planning period, such as 12 months.

- Calculate monthly amounts. Divide each target by the number of months available. Round up to the nearest €5 or €10 to create a small buffer.

- Add it to your monthly budget. Treat sinking fund contributions like a bill you pay to yourself. Do not wait to see what is left at the end of the month.

- Automate transfers. Set up a standing order just after payday. Automation removes the need for monthly willpower.

- Track balances. Use a spreadsheet, banking pots, envelopes, or a budgeting tool such as WhizBudget to see how much belongs to each category.

- Review quarterly. Every three months, check whether your estimates are still realistic. Adjust for new bills, price changes, or categories you forgot.

The most important step is automation. If you manually move money only when you remember, the system will be unreliable. A sinking fund works best when it becomes part of your normal payday routine.

Where to Keep Your Sinking Fund Money

Your sinking fund should be safe, easy to access, and separate from everyday spending. You are not investing this money for long-term growth. You are parking it until a known cost arrives.

Good options include:

- Instant-access savings account: Suitable for most sinking funds because you can withdraw when needed.

- Bank sub-accounts or pots: Many European banks and fintech apps allow separate spaces for goals such as car, holidays, and insurance.

- Separate current account: Useful if your bank does not offer pots, but you still want to keep the money away from daily spending.

- Cash envelopes: May work for small categories, but are less secure and less practical for large bills or online payments.

Avoid locking sinking fund money into accounts with withdrawal penalties unless you are certain you will not need it early. Also avoid investing short-term sinking funds in stocks or funds. If markets fall just before your insurance or school payment is due, you could be forced to sell at a loss.

If possible, earn some interest, but do not chase returns at the expense of access. The main job of a sinking fund is stability.

How to Prioritize Sinking Funds When Money Is Tight

If your budget is already stretched, seeing a list of sinking funds can feel overwhelming. Do not give up. You can start with the most urgent and essential categories first.

Use this priority order:

- Legal or compulsory costs: car insurance, property tax, required registration fees, and essential documentation.

- Essential living costs: home repairs, heating system maintenance, medical care, school basics, and transport needed for work.

- High-risk costs: car repairs if you depend on your vehicle, pet care if you have an older pet, or appliance replacement if an item is already failing.

- Quality-of-life costs: holidays, gifts, celebrations, hobbies, and non-essential subscriptions.

When money is tight, do not try to fully fund every category immediately. Instead, choose a starter amount. Even €10 or €20 per month toward a future bill is better than saving nothing.

You can also use the deadline method. Fund the categories with the nearest due dates first. For example, if school costs are due in two months and home insurance is due in ten months, school costs may need attention first.

If the total sinking fund amount is higher than you can afford, your budget is showing you a useful truth: some future costs need to be reduced, delayed, or planned differently. That might mean choosing a shorter holiday, buying second-hand school items, comparing insurance quotes before renewal, or spreading large purchases over a longer saving period. The goal is not vague advice like spend less. The goal is to match your future plans to your actual cash flow.

Example Sinking Fund Budget for a Real Household

Imagine a household in Ireland, Spain, Germany, or France with two adults, one child, one car, and a rented or mortgaged home. Their monthly income after tax is €3,800. Regular monthly bills, groceries, transport, and minimum debt payments total €3,150. That leaves €650 before irregular expenses, extra debt payments, and personal spending.

After reviewing the last year, they identify these irregular costs:

| Category | Annual Estimate | Monthly Sinking Fund | Notes |

|---|---|---|---|

| Car maintenance and tyres | €720 | €60 | Based on service, small repairs, and tyre replacement |

| Car insurance excess and renewal gap | €360 | €30 | Extra buffer for policy changes or excess |

| Home maintenance | €600 | €50 | Small repairs, appliance fund, boiler service |

| School costs | €600 | €50 | Books, trips, uniform, sports items |

| Medical and dental | €480 | €40 | Check-ups, prescriptions, dental cleaning |

| Christmas and gifts | €960 | €80 | Gifts, food, travel, events |

| Holiday | €1,200 | €100 | Accommodation, travel, spending money |

| Annual subscriptions | €240 | €20 | Software, memberships, streaming annual plans |

The total sinking fund contribution is €430 per month. This leaves €220 from the original €650 for extra debt payments, personal spending, or additional savings.

Before using sinking funds, this household may have thought they had €650 spare each month. In reality, €430 of that was needed for predictable future costs. Without a sinking fund, those costs would likely end up on a credit card or come from their emergency fund.

This is the power of an annual expenses budget. It turns an unclear surplus into a realistic plan.

Mistakes to Avoid When Managing Sinking Funds

Sinking funds are simple, but a few common mistakes can weaken the system.

- Using one vague savings account. If all money sits in one pot with no labels, it is easy to spend holiday money on car repairs and then be short later.

- Forgetting inflation and price increases. If last year cost €800, this year may cost €850 or €900. Review your numbers.

- Not saving until the bill is close. The sooner you start, the lower the monthly amount. Waiting until three months before an annual bill makes the contribution much harder.

- Confusing wants with essentials. A holiday fund is useful, but it should not come before legally required insurance or essential medical care.

- Raiding funds for daily spending. If you keep dipping into sinking funds for groceries or nights out, your monthly budget needs adjusting.

- Setting too many categories. Ten clear categories are usually better than forty tiny ones. Keep the system manageable.

- Ignoring one-off upcoming events. Weddings, moving costs, a new baby, or a major birthday may need temporary sinking funds.

Another mistake is expecting your first version to be perfect. It will not be. Your first year of sinking funds is partly a learning year. You will discover categories you missed and estimates that were too low. Adjust and continue.

Tools and Apps That Can Help Track Sinking Funds

You can track sinking funds in several ways. The best tool is the one you will actually use.

- Spreadsheet: Good for people who like control and simple formulas. Create columns for category, target, current balance, monthly contribution, and due date.

- Banking pots or spaces: Useful if your bank allows separate savings goals. You can visually separate money without opening many accounts.

- Budgeting app: Helpful if you want your monthly budget and sinking funds in one place. WhizBudget can help you plan categories, track balances, and see how irregular expenses affect your real monthly cash flow.

- Notebook or paper planner: Works if you prefer a physical system, but you must update it consistently.

Whichever tool you use, make sure it answers three questions quickly:

- How much do I need for this category?

- How much do I have saved right now?

- How much must I add each month to stay on track?

If your system cannot answer those questions, it is too unclear. Keep simplifying until it can.

FAQs

What is a sinking fund for irregular expenses?

A sinking fund for irregular expenses is money saved regularly for costs that do not happen every month. Examples include car repairs, insurance renewals, Christmas, school costs, holidays, and annual subscriptions.

How much should I put in a sinking fund each month?

Use the formula: expected cost divided by the number of months until it is due. If a bill is €600 and due in 12 months, save €50 per month. For uncertain costs, estimate based on previous years and round up slightly.

Should I have separate sinking funds for every expense?

Not necessarily. Separate categories are useful, but too many can become confusing. Group similar expenses, such as car costs, home maintenance, medical, gifts, school, holidays, and insurance.

Is a sinking fund the same as emergency savings?

No. A sinking fund is for expected or planned costs. Emergency savings are for serious unexpected events such as job loss, urgent essential repairs, or sudden income disruption. Both are important.

Where should I keep my sinking fund money?

Keep it in a safe and accessible place, such as an instant-access savings account, bank pots, or a separate current account. Avoid risky investments for money you will need within the next year or two.

What if I cannot afford all my sinking funds right now?

Start with the most essential and urgent categories. Prioritize compulsory bills, transport needed for work, housing, medical care, and school basics. Add smaller amounts to lower-priority funds when your budget allows.

Can sinking funds help with unexpected expenses savings?

Yes, but they do not replace an emergency fund. Sinking funds reduce the number of expenses that feel unexpected because you have planned for them. Your emergency fund can then be reserved for true emergencies.

Conclusion

Irregular expenses are not rare exceptions. They are a normal part of personal finance. If you do not plan for them, they will keep derailing your budget, draining your emergency fund, or pushing you toward debt.

A sinking fund gives every future bill a monthly plan. Start by reviewing your past spending, choose practical categories, calculate monthly amounts, automate transfers, and track your progress. Even if you begin with only a few categories, you will quickly feel more prepared and less reactive.

If you want a clearer way to manage sinking funds alongside your everyday budget, WhizBudget can help you organise categories, plan ahead, and make irregular expenses easier to handle. Build your first sinking fund today, and give your future bills a place in your budget before they arrive.

How to Build an Emergency Fund: Step-by-Step Guide

How to Build an Emergency Fund: Step-by-Step Guide

What is an Emergency Fund?

An emergency fund is a savings account specifically set aside to cover unexpected expenses or financial emergencies. These can include medical bills, car repairs, or sudden job loss. Having an emergency fund provides financial security and peace of mind.

Why You Need an Emergency Fund

Building an emergency fund is crucial for several reasons:

- Financial Security: It acts as a safety net, protecting you from sudden financial shocks.

- Peace of Mind: Knowing you have funds set aside reduces stress during uncertain times.

- Avoiding Debt: An emergency fund helps you avoid relying on credit cards or loans, which can lead to debt accumulation.

Steps to Build Your Emergency Fund

- Set a Savings Goal: Determine how much you need in your fund, typically 3 to 6 months’ worth of expenses.

- Open a Separate Savings Account: Keep your emergency fund separate from your regular accounts to avoid the temptation of spending it.

- Automate Your Savings: Set up automatic transfers to your emergency fund every month.

- Cut Unnecessary Expenses: Review your budget and identify areas where you can cut back to increase your savings.

- Increase Your Income: Consider side jobs or freelance work to boost your savings more quickly.

How Much Should You Save?

Most financial experts recommend saving three to six months’ worth of living expenses. For example, if your monthly expenses are €1,500, aim for an emergency fund of €4,500 to €9,000. Adjust based on your personal circumstances, job stability, and financial obligations.

Where to Keep Your Emergency Fund

Choose a savings account that offers easy access and minimal fees. Online banks often provide higher interest rates than traditional banks. Some good options include:

- High-yield savings accounts

- Money market accounts

- Short-term certificates of deposit (CDs)

Common Mistakes to Avoid

- Not Saving Enough: Underestimating your emergency fund needs can leave you vulnerable.

- Using the Fund for Non-Emergencies: Only use your emergency fund for true emergencies to maintain its purpose.

- Neglecting to Replenish: If you use the fund, make sure to replenish it as soon as possible.

FAQs

1. How quickly should I build my emergency fund?

Start saving as soon as possible. Aim to reach your goal within one to three years, depending on your financial situation.

2. Can my emergency fund earn interest?

Yes, consider placing your emergency fund in a high-yield savings account to earn interest over time.

3. Is it okay to invest my emergency fund?

It's best to keep your emergency fund in a liquid account for quick access, rather than investing it in volatile assets.

4. How do I know when to use my emergency fund?

Use your emergency fund for unexpected expenses that cannot be covered by your regular budget.

5. Can I use my emergency fund for planned expenses?

No, the purpose of an emergency fund is to cover unplanned expenses only.

6. How can WhizBudget help with my emergency fund?

WhizBudget is a helpful budgeting tool that allows you to track your savings goals and manage your finances effectively.

7. What if I exhaust my emergency fund?

If you use your emergency fund, prioritize rebuilding it as soon as possible to maintain financial security.

Conclusion

Building an emergency fund is a vital step in achieving financial stability. By following the steps outlined above and using tools like WhizBudget to track your progress, you can ensure that you are prepared for any unexpected expenses that may come your way. Start today, and take control of your financial future!

Micro-Saving Hacks That Add Up: 15 Tricks That Actually Work

What are the best micro-saving hacks that work?

The most effective micro-saving tricks include rounding up purchases, automating transfers, setting no-spend days, and using cashback apps. Small, consistent actions like these build up your savings over time, without feeling like a sacrifice.

Saving money doesn't always require big changes. Sometimes, it's the tiny tweaks to your everyday habits that make the biggest difference. These micro-saving strategies are easy to implement, stress-free, and proven to help people boost their savings with minimal effort.

Whether you're living paycheck to paycheck or just want to save more without noticing, these 15 micro-saving hacks will help you stay on track.

1. Round Up Your Purchases Automatically

Link your debit card to an app that rounds up your purchases to the nearest dollar and saves the change.

- Spend $3.45 → $0.55 goes to savings

- Works well with budgeting apps like Qapital or banking features that support this

- Set and forget style saving

2. Use the 24-Hour Rule Before Buying Non-Essentials

Impulse buying kills savings. This rule gives you time to reflect:

- Wait 24 hours before purchasing anything non-essential

- Helps eliminate emotional spending

- You’ll often find you don’t actually need it

3. Automate $1–$5 Daily Transfers

Set a small, daily transfer from checking to savings.

- Use your bank or app to automate it

- Feels insignificant day-to-day, but adds up fast

- Great for building your emergency fund

4. Cancel One Subscription Per Month

Chances are you’re overpaying for recurring services.

- Audit your subscriptions (streaming, fitness, apps)

- Cancel at least one unnecessary subscription monthly

- Redirect that money straight into savings

5. Take the No-Spend Day Challenge

Commit to one no-spend day per week:

- No coffee runs, takeout, or Amazon splurges

- Plan ahead with packed meals and offline activities

- Save $10–$30 per week with this one habit

6. Skim Your Account Weekly

Every Sunday, transfer the excess cash from your checking account:

- Anything above your target balance goes into savings

- Builds discipline and clears mental clutter

- Ideal for flexible savers who don’t want strict rules

7. Use Cashback Apps for Everyday Spending

Leverage rewards for things you already buy.

- Try Rakuten, Ibotta, or Honey

- Combine with coupons for double savings

- Transfer cashback directly to savings monthly

8. Set Micro Goals, Not Just Big Ones

Instead of “save $5,000,” break it down:

- Weekly goals like $20 or $30

- Check-in each week to track progress

- Celebrating small wins keeps motivation high

9. Save Windfalls, Not Spend Them

Got a bonus, gift, or tax refund?

- Save at least 50–80%

- Consider opening a high-yield savings account

- Pretend you never had it = easy savings

10. Trigger-Based Saving

Create fun “if this, then save” rules:

- Every time you eat out → save $5

- Every time it rains → save $2

- Use IFTTT or app-based rules to automate it

11. Opt for Generic Brands and Bank the Difference

Next grocery run:

- Choose store brands for basics (cereal, pasta, cleaners)

- Note the difference in price

- Transfer savings manually or via budgeting app like WhizBudget

12. Cash-Only Weekends

Spend only what you withdraw in cash.

- Leaves no room for overdrafting or tapping plastic

- Makes you more mindful of every dollar

- Any unused cash = savings

13. Unsubscribe from Retail Emails

Avoid temptation altogether.

- Clean your inbox of sales triggers

- Install email filters or use unroll.me

- Fewer ads = fewer impulse buys = more savings

14. Split Paychecks into Multiple Accounts

Direct deposit part of your paycheck into savings.

- Out of sight, out of mind

- Start with just 5–10%

- Most employers or banks support split deposits

15. Create a “Treat Fund” in Your Budget

Avoid blowing your entire budget on one bad day:

- Set aside a small “fun money” stash

- Keeps emotional spending in check

- Whatever’s leftover at month-end = move to savings

Conclusion

Micro-saving isn’t about restriction, it’s about working smarter with the money you already have. When you stack these small habits together, they create a solid, low-effort saving system.

Pick 2–3 of these micro-saving hacks today and test them out this week. You’ll be surprised how quickly your savings start to grow.

The 30-Day Money Detox: Save Without Spending

Have you ever checked your bank account and thought:

“Where the heck did my money go?”

Or maybe you feel like you should be saving, but every time payday hits, it’s like money just evaporates.

Groceries? $100.

One coffee? $6.

Blink twice? Somehow spent $50 on random Amazon junk.

You’re not alone.

This is exactly why the 30-Day Money Detox exists.

It’s not magic.

It’s not extreme.

It just works.

Let’s break it down.

What’s a 30-Day Money Detox?

It’s simple.

For 30 days, you stop spending on anything non-essential.

No takeout.

No random Target runs.

No "just browsing" on your favorite apps.

You only cover what you need to live:

- Rent or mortgage

- Groceries (real ones, not snacks and soda)

- Utilities

- Gas or public transport

- Medical needs

That’s it. The rest? You press pause.

This challenge resets your money habits, fast.

Why Do This?

Let’s be real:

Most of us don’t have a spending problem.

We have a leak problem.

Money slips out in small ways. Daily. Silently. Until you’re left wondering where your paycheck went.

The detox shows you how often you’re buying out of boredom, not need.

And yeah—it’s a bit uncomfortable.

But so is being broke.

What You’ll Get Out of It

By the end of 30 days, you’ll:

- Save hundreds (most people save $300–$1000+)

- Actually see where your money should go

- Kill off bad habits before they wreck your budget

- Feel in control again

You won’t get rich overnight.

But you will stop being confused about where your money’s going.

How to Start Your 30-Day No-Spend Challenge

Start simple.

1. Pick your start date

Tomorrow works. So does next Monday. Just start.

2. Set your “essentials-only” list

Write down what you’re allowed to spend on.

Don’t guess. Be clear.

Essentials = rent, bills, food, gas.

Non-essentials = everything else.

If you’re not sure, ask:

“Would I still need this if I lost my job today?”

If no, skip it.

3. Hide your cards. Delete the apps. Unfollow the temptation.

Make it hard to spend.

Amazon in your bookmarks? Gone.

Food delivery apps? Bye.

Insta influencers pushing $70 candles? Unfollowed.

4. Track everything

Use WhizBudget.

It’s built for this kind of thing.

No ads. No fluff.

Just track your cash, see where it’s leaking, and fix it.

Seriously—don’t try this without a budget app. You’ll fail. Fast.

Real Talk: What About Emergencies?

Emergencies happen. That’s life.

If something truly urgent pops up (car repair, sudden meds), handle it.

This isn’t prison.

It’s a detox.

Just don’t call a $9 smoothie an “emergency.”

Tips to Actually Stick With It

- Tell someone. Accountability helps. Post it. Text a friend. Even better—do it together.

- Use cash. Take out money for essentials. When it’s gone, it’s gone.

- Prep your meals. Fast food cravings hit hard at 7pm. Be ready.

- Say no. A lot. It’s awkward at first. Gets easier.

- Write down what you wanted to buy. Look at it at the end of 30 days. Half of it won’t matter anymore.

But What If I Fail?

You will.

Everyone slips.

The point isn’t to be perfect.

It’s to wake up and start paying attention again.

Miss a day? Cool.

Don’t quit.

Keep going.

What Happens After 30 Days?

That’s up to you.

You might:

- Feel way more confident with your money

- Keep your new habits

- Build an emergency fund

- Start saving for stuff that matters (not impulse buys)

But one thing’s for sure:

You’ll never look at spending the same again.

Ready to Try It?

You don’t need willpower.

You need a plan.

Use WhizBudget to set up your essentials list, track your no-spend days, and see exactly where your cash is going.

It’s free. It’s simple. It works.

Because if your money’s been running you…

It’s time to flip the script.

The 50/30/20 Rule: How to Save Money Without Feeling Restricted

Have you ever tried saving money but felt like you were constantly depriving yourself? I’ve been there. Budgeting can feel overwhelming, but I discovered a simple rule that changed everything, the 50/30/20 rule. It’s an easy framework that helps you manage your money without feeling like you're cutting out all the fun.

What Is the 50/30/20 Rule?

The 50/30/20 rule is a budgeting method that divides your income into three categories:

50% for Needs: Essentials like rent, utilities, groceries, insurance, and minimum debt payments.

30% for Wants: The fun stuff, dining out, entertainment, travel, and hobbies.

20% for Savings & Debt Repayment: Emergency funds, retirement contributions, investments, and paying off extra debt.

It’s simple, flexible, and realistic. Instead of tracking every single expense, you just allocate your income into these three buckets.

Why It Works

Before using this rule, I felt guilty about spending money on things I enjoyed. Either I was saving too aggressively and feeling deprived, or I was overspending and feeling guilty. The 50/30/20 rule struck the perfect balance. It allowed me to prioritize my needs, enjoy my wants, and still make progress toward financial goals.

How to Implement It

Calculate Your After-Tax Income: Take your monthly paycheck after taxes and deductions.

Break It Down: Multiply your income by 50%, 30%, and 20% to determine how much goes into each category.

Adjust as Needed: Your situation might be different. If your needs exceed 50%, try cutting back on wants. If you’re paying off debt aggressively, your savings percentage may be lower temporarily.

Automate & Track: Set up automatic transfers for savings and track expenses with a budgeting app, eg WhizBudget

The Bottom Line

Saving money doesn’t have to mean sacrificing joy. The 50/30/20 rule gives you structure while allowing you to live your life. If you’ve struggled with budgeting, try this method, it might just change the way you think about money.

Automate Your Savings and Build Wealth Effortlessly

Saving money can feel like a challenge, especially when life’s expenses keep piling up. However, by automating your savings, you can make wealth-building an effortless habit rather than a daunting task. In this guide, we’ll walk you through simple yet effective ways to automate your savings and set yourself up for long-term financial success.

Why Automate Your Savings?

Automation takes the guesswork out of saving. Instead of relying on willpower to set money aside, automation ensures you consistently save without having to think about it. This approach provides consistency, helps you avoid temptation, reduces stress, and capitalizes on compound interest. Regular contributions add up over time, making it easier to build wealth effortlessly. Since the money is saved before you have a chance to spend it impulsively, you are more likely to stay on track. Additionally, automating savings eliminates the stress of remembering to set money aside manually, and the earlier you start, the more you benefit from compound growth.

Steps to Automate Your Savings

Setting up direct deposits into a savings account is one of the easiest ways to start automating your savings. Many employers allow you to split your direct deposit between multiple accounts, making it simple to allocate a fixed percentage for savings before you even see the money. If your employer doesn’t offer paycheck splitting, you can set up automatic transfers from your checking account to your savings account. Most banks allow you to schedule recurring transfers weekly, bi-weekly, or monthly, ensuring that saving becomes a regular habit.

Using a high-yield savings account can help maximize your savings since these accounts offer higher interest rates than traditional savings accounts, allowing your money to grow faster over time. Another strategy is automating retirement contributions. If your employer offers a 401(k), setting up automatic deductions from your paycheck can be beneficial, especially if there is a company match. For those without a 401(k), setting up automatic monthly contributions to a Roth or Traditional IRA can help grow retirement savings effortlessly.

Round-up savings apps such as Acorns, Qapital, and Digit are also helpful tools for automating savings. These apps round up your purchases to the nearest dollar and save the spare change for you. Over time, these small savings add up significantly. Additionally, using a robo-advisor or automated investment platform can help grow your wealth. These services automatically invest your money based on your financial goals and risk tolerance, helping you build long-term wealth passively.

While not directly related to saving, automating bill payments can ensure you never miss a due date. This prevents late fees and protects your credit score, which can save you money on interest rates in the future.

Automating your savings is one of the simplest yet most effective ways to build wealth without extra effort. By setting up direct deposits, automatic transfers, and utilizing savings and investment apps, you can ensure consistent financial growth. Start small if needed, but take action today, your future self will thank you!

Sinking Funds Explained: The Smart Way to Budget for Future Expenses

Unexpected expenses can throw even the best budget off track. That’s where sinking funds come in. They help you plan for known, but irregular, expenses so you’re never caught off guard.

A sinking fund is a dedicated savings strategy where you regularly set aside money for anticipated future expenses, allowing you to make significant purchases without incurring debt.

Unlike an emergency fund, which is for unexpected financial surprises, sinking funds are designed for predictable costs, like holiday gifts, car repairs, home maintenance, or annual insurance premiums. By setting aside small amounts regularly, you can avoid the stress of large, one-time payments.

Setting up a sinking fund is simple. Start by identifying expenses that don’t occur monthly but still need to be covered. Then, estimate the total cost and divide it by the number of months until the expense is due. For example, if you need $600 for holiday gifts in six months, setting aside $100 per month makes it manageable.

Sinking funds work best when they are separated from your main checking account. Consider using a high-yield savings account, a budgeting app or WhizBudget to keep track of your funds. Some people prefer multiple accounts for different categories, while others use a spreadsheet or cash envelopes to manage their savings.

Common sinking fund categories include:

Car maintenance

Home repairs

Medical expenses

Travel and vacations

Insurance premiums

Holiday and birthday gifts

The key to making sinking funds work is consistency. Even if you can only contribute small amounts at first, the habit of saving will add up over time. When the expense finally arrives, you’ll be prepared, and your budget will remain intact.

Sinking funds are a simple yet powerful way to take control of your finances and avoid debt. By planning ahead, you can handle future expenses with confidence and financial peace of mind.

Want more budgeting tips? Explore our blog for smart financial strategies!

Emergency Funds: How Much Should You Really Save?

Life is unpredictable, and unexpected expenses can arise at any moment. Whether it's a medical emergency, job loss, or sudden car repairs, having an emergency fund can be the key to financial stability. But how much should you save? Let’s break it down.

You can use our free emergency fund calculator or just keep reading below.

Why an Emergency Fund is Essential

An emergency fund is a financial cushion that helps you cover urgent expenses without relying on credit cards or loans. Here’s why it’s crucial:

Prevents Debt: Avoid high-interest loans during financial crises.

Reduces Stress: Peace of mind knowing you have a backup plan.

Protects Long-Term Savings: Keeps you from dipping into retirement or investment accounts.

How Much Should You Save?

The amount you need depends on your financial situation, income stability, and lifestyle. Consider these guidelines:

Minimum Savings: Start with at least $1,000 to cover minor emergencies.

Three to Six Months of Expenses: This is the general recommendation for most households.

More Than Six Months: If you have an unstable income, are self-employed, or have dependents, aim for 6–12 months of essential expenses.

How to Build Your Emergency Fund

Set a Goal: Calculate your monthly essential expenses and multiply them by your target months.

Start Small: Even saving $20–$50 per week can add up over time.

Automate Savings: Set a direct deposit into a dedicated emergency fund account.

Cut Unnecessary Expenses: Redirect money from non-essential spending into your fund.

Use Windfalls Wisely: Tax refunds, bonuses, or extra income can give your savings a boost.

Where to Keep Your Emergency Fund

Your emergency fund should be easily accessible but separate from your daily spending account. Ideal options include:

High-Yield Savings Accounts: Earn interest while keeping funds liquid.

Money Market Accounts: Offer a balance of accessibility and returns.

Traditional Savings Accounts: A simple, secure place to store cash.

When to Use Your Emergency Fund

Use your emergency fund only for genuine financial emergencies, such as:

Unplanned medical expenses

Major car or home repairs

Sudden job loss or income reduction

Urgent travel for family emergencies

An emergency fund is a financial lifeline that protects you from the unexpected. Start small, stay consistent, and build a safety net that provides peace of mind. By planning ahead, you can face financial challenges with confidence and stability.

Ready to take control of your financial future? Start building your emergency fund today! WhizBudget is here to help you keep track!

Trending Topics

Recent Posts

How to Build an Emergency Fund: Step-by-Step Guide

Jul 01, 2026

The 30-Day Money Detox: Save Without Spending

Apr 05, 2025

Automate Your Savings and Build Wealth Effortlessly

Jan 25, 2025